Dries Buytaert

Blog

Projects

Photos

About

Search

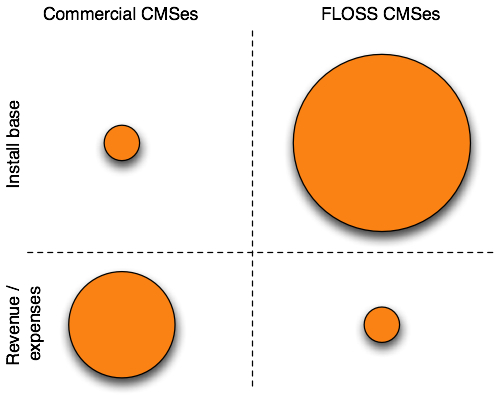

CMS marketplace

№ 220

APR 13, 2007

What is wrong with this picture?

Brain teaser.