Digital Distributors vs Open Web: who will win?

Contents

I've spent a fair amount of time thinking about how to win back the Open Web, but in the case of digital distributors (e.g. closed aggregators like Facebook, Google, Apple, Amazon, Flipboard) superior, push-based user experiences have won the hearts and minds of end users, and enabled them to attract and retain audience in ways that individual publishers on the Open Web currently can't.

In today's world, there is a clear role for both digital distributors and Open Web publishers. Each needs the other to thrive. The Open Web provides distributors content to aggregate, curate and deliver to its users, and distributors provide the Open Web reach in return. The user benefits from this symbiosis, because it's easier to discover relevant content.

As I see it, there are two important observations. First, digital distributors have out-innovated the Open Web in terms of conveniently delivering relevant content; the usability gap between these closed distributors and the Open Web is wide, and won't be overcome without a new disruptive technology. Second, the digital distributors haven't provided the pure profit motives for individual publishers to divest their websites and fully embrace distributors.

However, it begs some interesting questions for the future of the web. What does the rise of digital distributors mean for the Open Web? If distributors become successful in enabling publishers to monetize their content, is there a point at which distributors create enough value for publishers to stop having their own websites? If distributors are capturing market share because of a superior user experience, is there a future technology that could disrupt them? And the ultimate question: who will win, digital distributors or the Open Web?

I see three distinct scenarios that could play out over the next few years, which I'll explore in this post.

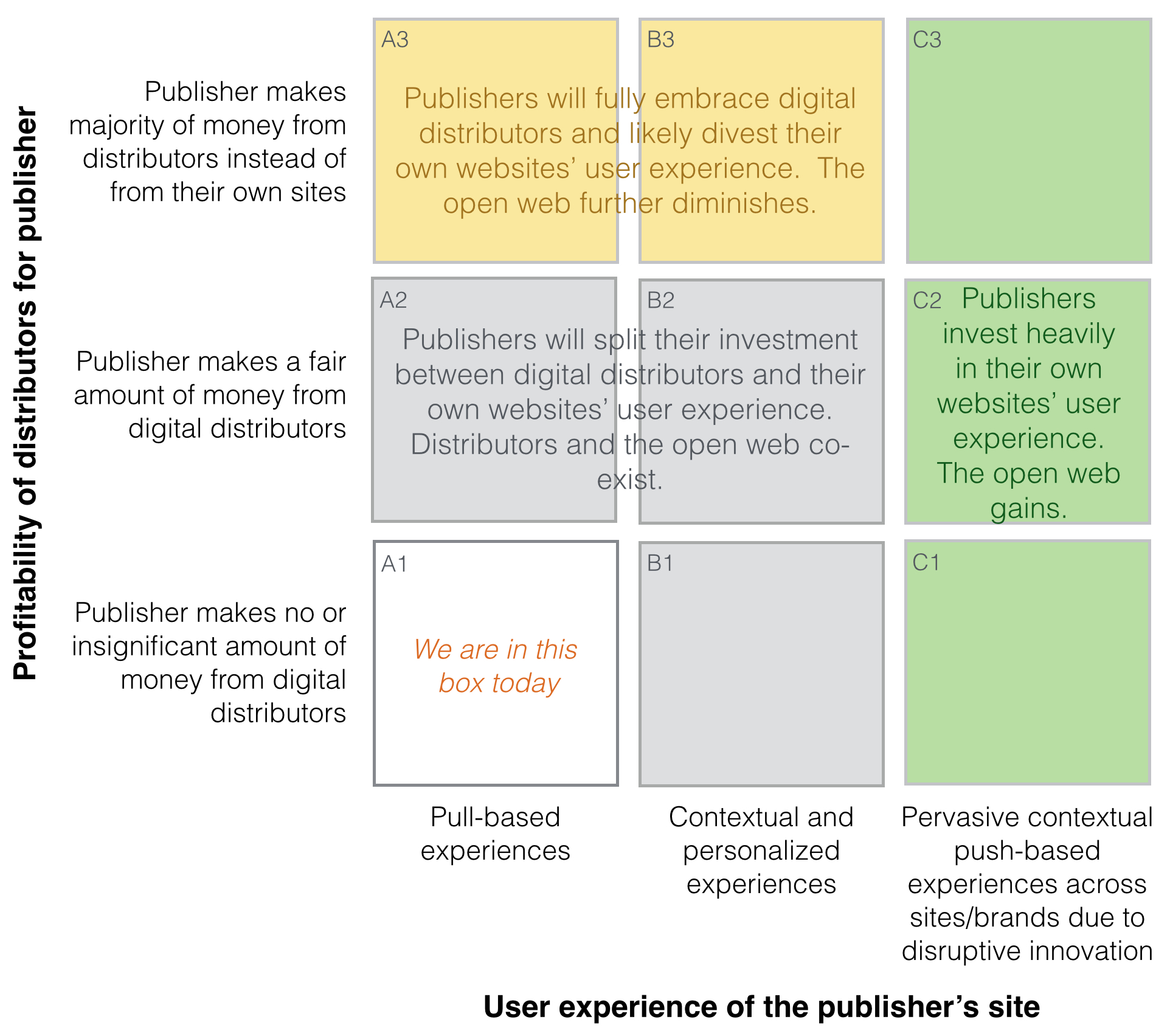

§Scenario 1: Digital distributors provide commercial value to publishers (A1 → A3/B3)

Digital distributors provide publishers reach, but without tangible commercial benefits, they risk being perceived as diluting or even destroying value for publishers rather than adding it. Right now, digital distributors are in early, experimental phases of enabling publishers to monetize their content. Facebook's Instant Articles currently lets publishers retain 100 percent of revenue from the ad inventory they sell. Flipboard, in efforts to stave off rivals like Apple News, has experimented with everything from publisher paywalls to native advertising as revenue models. Expect much more experimentation with different monetization models and dealmaking between the publishers and digital distributors.

If digital distributors like Facebook succeed in delivering substantial commercial value to the publisher they may fully embrace the distributor model and even divest their own websites' front-end, especially if the publishers could make the vast majority of their revenue from Facebook rather than from their own websites. I'd be interested to see someone model out a business case for that tipping point. I can imagine a future upstart media company either divesting its website completely or starting from scratch to serve content directly to distributors (and being profitable in the process). This would be unfortunate news for the Open Web and would mean that content management systems need to focus primarily on multi-channel publishing, and less on their own presentation layer.

As we have seen from other industries, decoupling production from consumption in the supply-chain can redefine industries. We also know that introduces major risks as it puts a lot of power and control in the hands of a few.

§Scenario 2: The Open Web's disruptive innovation happens (A1 → C1/C2)

For the Open Web to win, the next disruptive innovation must focus on narrowing the usability gap with distributors. I've written about a concept called a Personal Information Broker (PIM) in a past post, which could serve as a way to responsibly use customer data to engineer similar personal, contextually relevant experiences on the Open Web. Think of this as unbundling Facebook where you separate the personal information management system from their content aggregation and curation platform, and make that available for everyone on the web to use. First, it would help us to close the user experience gap because you could broker your personal information with every website you visit, and every website could instantly provide you a contextual experience regardless of prior knowledge about you. Second, it would enable the creation of more distributors. I like the idea of a PIM making the era of handful of closed distributors as short as possible. In fact, it's hard to imagine the future of the web without some sort of PIM. In a future post, I'll explore in more detail why the web needs a PIM, and what it may look like.

§Scenario 3: Coexistence (A1 → A2/B1/B2)

Finally, in a third combined scenario, neither publishers nor distributors dominate, and both continue to coexist. The Open Web serves as both a content hub for distributors, and successfully uses contextualization to improve the user experience on individual websites.

§Conclusion

Right now, since distributors are out-innovating on relevance and discovery, publishers are somewhat at their mercy for traffic. However, a significant enough profit motive to divest websites completely remains to be seen. I can imagine that we'll continue in a coexistence phase for some time, since it's unreasonable to expect either the Open Web or digital distributors to fail. If we work on the next disruptive technology for the Open Web, it's possible that we can shift the pendulum in favor of "open" and narrow the usability gap that exists today. If I were to guess, I'd say that we'll see a move from A1 to B2 in the next 5 years, followed by a move from B2 to C2 over the next 5 to 10 years. Time will tell!

Join 5,000+ readers. I'm the creator of Drupal and co-founder of Acquia. I write about Open Source, AI, and the future of the web, with a focus on building, scaling, and thinking long-term.